Because the CFPB is still a young agency, having formed in 2011 pursuant to the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (Dodd-Frank), the enforcement record of the Agency is somewhat limited, not by effort or action, but by historical time constraints. But make no mistake, youth should not be confused with regulatory patience. The CFPB has and continues to be aggressive and exuberant in pursuing high-profile enforcement actions, and considers itself, as of 2016, to be "fully functional" as an agency.

From a compliance perspective, aggression and unpredictability are an unsettling combination. Given the lack of deep historical enforcement trend data, proactive businesses and their counsel cannot simply look to the past, they must also attempt to predict the future. Proactive compliance best practices therefore include not only consideration of the CFPB's policy priorities, new rulemaking and prior enforcement actions, but also re-examination of those areas of the law within the CFPB's jurisdiction that remain unsettled. To that end, insight into the possible new frontiers of CFPB enforcement and oversight can be found, in part, through consideration of the CFPB's use of amicus briefs.

It has been widely documented that the submission of amicus briefs (a brief filed by a non-party to the case, usually with some sort of expertise on a particular issue) to the United States Supreme Court, as well as the citation to those amicus briefs by the Supreme Court, are both trending upwards. An average of 14 amicus briefs per decided case were filed in during the 2012-2013 Supreme Court term. The 2014-2015 Supreme Court term broke a number of amicus brief records, including the most briefs filed in a single case and the most signatories on a single brief. Given the increasing frequency and perceived influence of the amicus brief, it is not surprising that the CFPB has implemented its own amicus briefing program, using that program to advance its policy objectives.

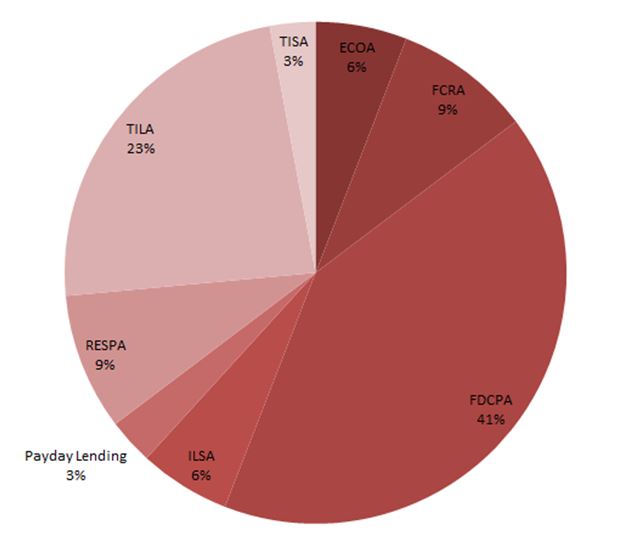

Through the date of this article, the CFPB has filed a total of 34 amicus briefs in state and federal courts, including nine amicus briefs the United States Supreme Court. Figure 1.1 represents a breakdown of all CFPB amicus briefs by area of law from 2011-present:

CFPB Amicus Briefs by Area of Law

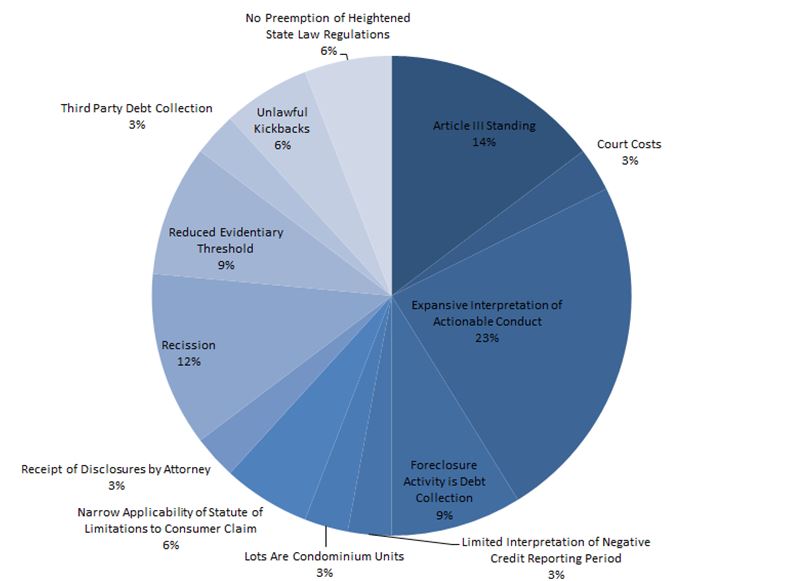

Figure 1.2 shows a breakdown of all CFPB amicus briefs by topic, regardless of governing law, from 2011-present:

CFPB Amicus Briefs by Topic

Looking behind the data, an interesting miniature trend emerges. While the CFPB has traditionally filed amicus briefs in cases involving the interpretation of conduct, e.g., does x conduct constitute a violation of y statute or rule, its most recent briefing suggests a willingness to decentralize some of its regulatory power by actively bolstering efforts to create or sustain new private causes of action under TILA, FCRA, FDCPA, and by taking the view that its regulatory and enforcement powers do not necessarily pre-empt similar or parallel state law claims. In fact, three of the last four amicus briefs filed by the CFPB were in support of private Article III standing under federal consumer protection laws.

Does this recent shift in amicus briefing suggest that the CFPB intends to throttle back in certain areas, ceding compliance to state governments or private individuals? That would seem unlikely. Instead, the focus on consumer standing reflects that an agency has matured and become more assured of the limits of its jurisdiction and powers. The emphasis on private standing, as a practical matter, can also be attributed to the fact that the Supreme Court recently considered and decided an important Article III case, Spokeo, Inc. v. Robins, remanding the case to the 9th Circuit for additional consideration of the Plaintiff's standing under the FRCA. The CFPB has been active in filing amicus briefing explaining its view of Spokeo and supporting the arguments made by private plaintiffs that they have met the concrete and particularized injury requirements of Article III.

Ultimately, when evaluating compliance and risk associated with business practices falling under the CFPB's jurisdiction, it is critical to view the issue not only as one that invokes administrative penalties, but as a matter that has the potential to spawn expensive, private civil litigation as well, even where current case law does not necessarily support or suggest a private cause of action. Increasingly, these new and creative claims will be legitimized and backed by the regulatory gravitas of the CFPB. Understanding the intersection of administrative and civil law in these areas will be essential in navigating the post Dodd-Frank landscape.