The United States Supreme Court recently rendered a decision in Salman1 resolving a circuit split over whether the government prosecuting an insider trading case must show that the person giving an insider tip received something of pecuniary value in return. Although the Court resolved the narrow question before it, the decision ultimately leaves us with more uncertainty than reassurance.

A. Background

The laws concerning insider trading are relatively well-established. A corporate insider owes a fiduciary duty to a publicly traded company not to exploit knowledge of the company's non-public information for personal benefit. This duty is breached when that insider trades in the securities of the company on the basis of material, non-public information. Similarly, a person receiving inside information (the "tippee") from the insider (the "tipper") acquires the tipper's fiduciary duty and breaches this duty by trading in the securities of the company with knowledge of the tipper's improper disclosure.

However, prior to the Salman opinion, there existed a circuit split over what personal benefit the tipper must receive from the tippee in order to be found liable for insider trading. The U.S. Supreme Court held in Dirks2 that a personal benefit may be inferred where the tipper receives something of value in exchange for the tip or "makes a gift of confidential information to a trading relative or friend." Calling this into question, the Second Circuit Court of Appeals in Newman3 interpreted the Dirks ruling narrowly and held that in order to infer a personal benefit, the exchange must "represent[] at least a potential gain of a pecuniary or similarly valuable nature" to the tipper. This conflict set the stage for the issue presented in the Salman case.

B. Salman v. United States

In Salman, an investment banker gave inside information to his brother. The brother then gave the information to his brother-in-law ("Salman"), who knew the information was not public and that it came from the investment banker. Salman then used the information to trade in the securities of the company. The crux of the dispute in Salman was over whether the investment banker received "value" or "a personal benefit" in exchange for the tip to his brother. After being initially convicted of insider trading, Salman sought to overturn this conviction on the basis that his tipper (the investment banker) did not personally receive money or property in exchange for the tip and thus did not obtain a personal benefit.

Salman's conviction was upheld by the Ninth Circuit Court of Appeals which, relying on Dirks, held that the relationship between the investment banker and his brother was sufficiently close to infer that the investment banker received a personal benefit. The Ninth Circuit also specifically rejected the Second Circuit's approach in Newman, requiring the tipper to receive something of pecuniary value in exchange for the tip.

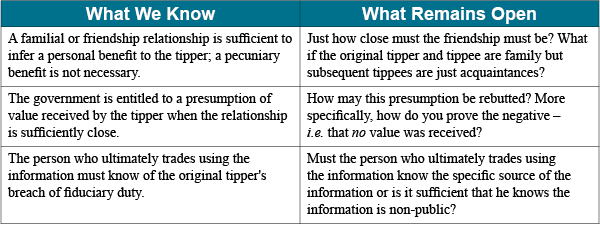

The United States Supreme Court sided with the Ninth Circuit in upholding Salman's conviction. Specifically, the Court relied upon language in Dirks that "[t]he elements of fiduciary duty and exploitation of non-public information also exist when an insider makes a gift of confidential information to a trading relative or friend." In other words, a tipper receives value or a personal benefit when he makes a "gift" of non-public information to a relative. The Court found that the analysis in Dirks clearly applied to the circumstances here: the investment banker (the tipper) provided inside information to a close relative, his brother (the tippee), and thereby breached his duties to the company. The Court also found that Salman acquired this duty, and breached it himself, by trading on the information with full knowledge that it had been improperly disclosed by the investment banker.

Although the Court sufficiently answered the question at hand – whether the tipper must receive pecuniary value or whether a familial relationship is sufficient to infer value received – the Court left significant lingering questions:

C. Conclusion

Because the Salman opinion was the first time the Supreme Court issued an insider trading opinion in nearly two decades, it may be a while before we have specific answers to these questions. In the interim, we will have to see how lower courts tackle these issues. In any event, it is clear that the Salman opinion lowers the burden government prosecutors will face when charging insider trading in cases involving family and friends. In light of this, compliance departments should be vigilant in establishing policies and procedures, and training insiders on safeguarding their company's material, non-public information, especially in the context of communication with family and friends.

If you have any questions regarding these issues or any other securities-related matters, please contact one of the attorneys in Baker Donelson's Government Enforcement and Investigations or Broker-Dealer/Registered Investment Adviser groups.

1Salman v. United States, 137 S. Ct. 420, 422 (2016).

2Dirks v. S.E.C., 103 S.Ct. 3255 (1983).

3United States v. Newman, 773 F.3d 438, 452, cert. denied, 577 U.S. _______, 136 S.Ct. 242, 193 L.Ed.2d 133.