UPDATED: March 31, 2020: According to the U.S. Treasury, small businesses can apply for Paycheck Protection Program (PPP) loans through existing SBA lenders starting April 3, 2020. Other lenders may apply to the SBA to be included as an approved lender starting April 10, 2020. You should consult with your local lender as to whether it is participating in the program.

ORIGINAL ARTICLE: On Friday, March 27, 2020, President Donald J. Trump signed into law the Coronavirus Aid, Relief, and Economic Security Act (the CARES Act), which among other COVID-19 relief items, provides $349 billion in Paycheck Protection Program loans for small businesses as well as other businesses and non-profit organizations that meet certain criteria. Prior to the passage of the CARES Act, Disaster Declarations made available separate small business loans through the Small Business Administration (SBA) Economic Injury Disaster Loan Program (EIDL).

SBA programs typically focus on the size of the business, which usually is based on number of employees or annual receipts. Unless an exception applies, a business concern must also identify and include the number of employees or annual receipts of each of its affiliated companies when determining its own size. This is an important consideration for any business that has outside investors or management, including venture capital investment. We have previously addressed these new loan programs here, here, and here. Businesses should consider the following regulations to evaluate eligibility under the applicable SBA size standards, including the affiliation requirements.

Size Eligibility Requirements for SBA Loans

Paycheck Protection Program (PPP)

The newly implemented PPP included in the CARES Act provides that during the covered period of February 15 through June 30, 2020, "in addition to small business concerns," any business concern, non-profit organization, veterans organization, or tribal business shall be eligible to receive a covered loan if that entity employs not more than the greater of:

- 500 employees; or

- the number of employees allowed by the employee-based size standard applicable to that entity.

In addition to the current allowable uses of SBA Section 7(a) Small Business Loans, proceeds from the PPP loans can be used for:

- Payroll costs;

- Insurance premiums and group health care benefits;

- Employee compensation;

- Payment of interest on mortgage obligations;

- Rent;

- Utilities; and

- Interest on debt.

The loan can be forgiven if used for the above purposes. Loans under the PPP program also do not require any personal guarantee or collateral from the borrower.

Businesses in the Accommodation and Food Services Industries

Businesses with the NAICS Code beginning with 72, such as restaurants and hotels, receive further expansions of eligibility for PPP. For example, the CARES Act provides that accommodation and food services industry companies with more than one physical location are eligible to receive the covered loans so long as they employ less than 500 employees at each physical location. Therefore, a restaurant company exceeding the 500-employee limit would still qualify for this program so long as it has no single location exceeding 500 employees.

The CARES Act also waives SBA's affiliation provisions (discussed below) for any business in the accommodation and food services industries with not more than 500 employees as of the date on which the loan is disbursed, any business concern operating as a franchise that has received a franchise identifier code from SBA, and any business that receives financial assistance from a Small Business Investment Corporation (SBIC).

Confirm Eligibility and Contact Your Lender Now

PPP loans under the CARES Act will be disbursed by banks directly to borrowers, not by the SBA itself. Therefore, SBA will need to create and issue final rules before banks will make PPP loans. The SBA's interpretation of the CARES Act language stating "in addition to small business concerns" could be an interesting development as final rules are developed. By a clear reading of the statute, the PPP program should be available to businesses that meet the above employee count criteria "in addition to small business concerns" that qualify under SBA's other regulations (i.e., annual receipts), even though they may exceed 500 employees. An open question exists about how SBA will implement that language. While banks cannot make these loans until they know the final rules, businesses should not wait until the final implementation of SBA's regulations to contact their lenders. Businesses would be wise to contact their lenders now to express their interest. Businesses can use the SBA's Lender Match program to find lenders who currently participate in the SBA loan program.

Economic Injury Disaster Loan Program (EIDL)

SBA's regulations at 13 CFR 123.300, et. seq. describe who is eligible for SBA's EIDL loans and confirm that EIDL loans are available only if the organization was a small business or a private non-profit organization at the time the declared disaster commenced. Under SBA's size regulations, it confirms that an applicant must meet the following two criteria to be a small business eligible for EIDL loans:

- Size of the applicant alone (without affiliates) must not exceed the size standard designated for the industry in which the applicant is primarily engaged; and

- Size of the applicant combined with its affiliates must not exceed the size standard designated for either the primary industry of the applicant alone or the primary industry of the applicant and its affiliates, whichever is higher. These size standards are set forth in §121.201.

EIDL loans offer up to $2 million in assistance, carry an interest rate of 3.75 percent, and have a maximum term of 30 years.

SBA Definition of a Small Business Concern

The SBA loan programs rely, in part, on SBA's size regulations to determine eligibility. Therefore, it is important to first confirm how the SBA defines a small business concern when evaluating eligibility. A "small business concern" under SBA's regulations is:

- Business entity that is organized for profit, with a place of business located in the U.S., and that operates primarily in the U.S. or makes a significant contribution to the U.S. economy through payment of taxes or use of American products, materials, or labor. Absent a few exceptions, most for-profit businesses with an active location in the U.S. will have little or no difficulty meeting this requirement; and

- Is also small under the particular size standard that corresponds to the North American Industrial Classification (NAICS) Code applicable to that business.

NAICS Codes are used by the federal government to track and report on the U.S. economy by segregating businesses into certain industry classifications. SBA uses the NAICS Code system simply to establish what businesses are small for purposes of SBA programs by assigning size standards to each particular NAICS Code. For example, the NAICS Code for "Full-Service Restaurants" (7222511) has an $8 million annual receipts-based size standard. As discussed below, this means that any full-service restaurant that is a "business concern" with average annual receipts of $8 million or less over the previous three years (for loan programs) is a small business concern under SBA's regulations. SBA's regulations at 13 C.F.R. § 121.201 provide a table identifying each NAICS Code and its associated size standard.

Employee-Based Sized Standards

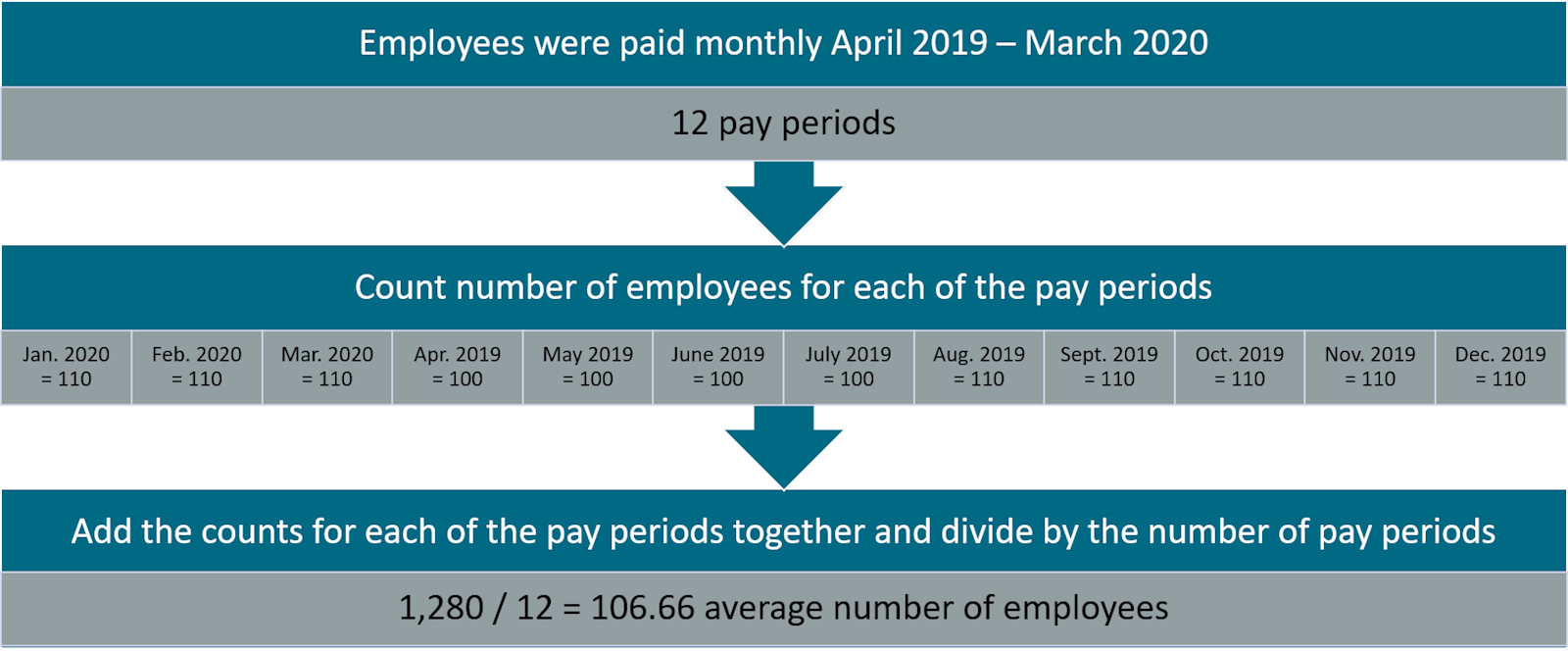

SBA's size standards are based on either the number of employees of the concern or the amount of average annual receipts. To determine the number of employees, a concern needs to calculate the average number of employees of the business (including the number of employees of its domestic and foreign affiliates) based upon the numbers of employees for each of the pay periods for the preceding completed 12 calendar months.

For example, if employees are paid monthly, there are 12 pay periods. The business needs to count the number of employees for each of those separate 12 pay periods, add the numbers from each of those pay periods together to create the total, and then divide that total by 12 to determine the average number of employees.

SBA counts all individuals employed on a full-time, part-time, or other basis. This includes employees from temp agencies. However, volunteers (i.e., individuals who receive no compensation, including no in-kind compensation, for work performed) are not considered employees. SBA will consider the totality of the circumstances, including criteria used by the IRS for federal income tax purposes, when determining whether individuals are employees of a concern or independent contractors.

To count the average number of employees of affiliated companies, the average number of employees of each affiliate is added to the average number of employees of the relevant business concern. Please see 13 C.F.R. § 121.106 to evaluate further how SBA counts the average number of employees.

Notably, the PPP program in the CARES Act does not use the word "average" when addressing the number of employees, but instead just states "500 employees." However, if the PPP is consistent with other SBA programs based on number of employees, it will use the above calculating procedures. The SBA also will use its existing regulations to determine eligibility for the EIDL program as provided in 13 C.F.R. § 121.301(a)(1) and 13 CFR 123.300, et. seq.

Size Standards Based on Annual Receipts

An entity's "annual receipts" for SBA's size calculations are generally considered the "total income" (or in the case of a sole proprietorship "gross income") plus "cost of goods sold" as these terms are defined and reported on IRS tax return forms.

For businesses that have existed for three or more years, annual receipts for Business Loan and Disaster Loan Programs means the total receipts of the concern over its most recently completed three fiscal years, divided by three. Essentially, it involves adding the annual receipts together over the three-year period and then dividing by three. The average annual receipts of a business concern with affiliates is calculated by adding the average annual receipts of the business with the average annual receipts of each affiliate.

As noted above, all of the public proclamations from Congress related to the PPP are focused on the employee count measurement, but the actual language in the CARES Act uses the term "in addition to small business concerns." This leaves an open question about whether the PPP loans should be available to small businesses under an annual receipts-based size standard, even if they exceed the maximum number of employees set forth in the CARES Act. SBA will likely clear that up in the near future when it issues regulations for the PPP. Annual receipts, however, are significant for the EIDL program as provided in 13 C.F.R. § 121.301(a)(1) and 13 CFR 123.300, et. seq.

The relevant regulations at 13 C.F.R. § 121.104(c)(4) (annual receipts) and 13 C.F.R. § 121.106 (number of employees) provide further background on how to calculate these numbers, including for businesses that have existed for a shorter time than the measuring period. They also further describe how affiliation principles need to be considered when confirming these numbers.

SBA Affiliation Rules for Calculating a Concern's Size

SBA's affiliation rules confirm whether the annual receipts or number of employees of other entities need to be added to the applicant's numbers when determining size. Outside of a few exceptions listed in the CARES Act and noted below, affiliation must be considered when evaluating eligibility for SBA loans. 13 C.F.R. § 121.301(f)(8). Therefore, unless an exception applies, a business determining its size must identify and include the annual receipts or number employees of its affiliates when determining whether it meets the applicable size standard.

Common Ways to Determine Affiliation and COVID-19 Exceptions

SBA concludes that "[c]oncerns and entities are affiliates of each other when one controls or has the power to control the other, or a third party or parties controls or has the power to control both." 13 C.F.R. § 121.301(f). We have provided below four of the most common ways in which SBA finds affiliation.

- Affiliation Based on Ownership

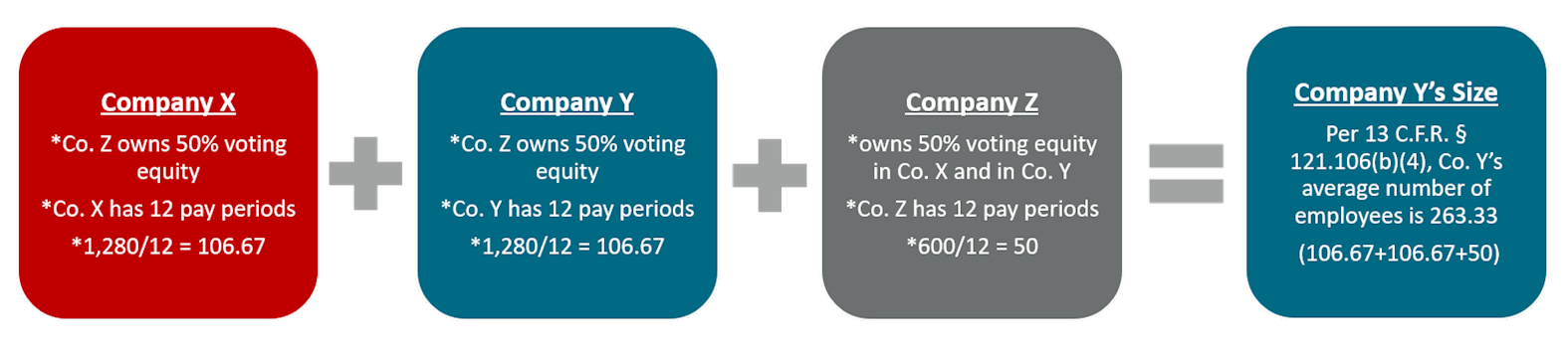

A concern or person owning 50 percent or more of another concern's voting equity is the most straight forward affiliation analysis. A business "is an affiliate" of an individual, concern, or entity that owns or has the power to control more than 50 percent of the concern's voting equity.

For example, if company Z solely owns 50 percent or more of each of company X and Y's voting equity, and company Y is determining its size under an employee-based size standard, company Y must include the number of employees of X, Y, and Z as part of the calculation. The employees of X, Y, and Z must all be included in company Y's number of employees because company Z controls both companies X and Y through its 50 percent or more ownership of those entities. Since company Z controls company Y, company Y also is affiliated with every other business that company Z controls.

Significantly, stock options, convertible securities, and agreements to merge have "present effect on the power to control the concern" when evaluating affiliation. Therefore, if an entity has stock options that would allow its equity interest to meet or exceed 50 percent of the concern's voting equity, it will be deemed to presently hold the 50 percent and control the business even though the options are not yet exercised. The "present effect" rule applies to any "agreement in principle," which can cause difficult questions about letters of intent and similar agreements.

Finally, for SBA loan programs, if no individual, concern, or entity is found to control 50 percent or more of the voting equity, then SBA will deem the board of directors or president or CEO (or other officers, managing members, or partners who control the management) to be in control of the concern.

- Affiliation Based on Management

Affiliation also "arises" when the management of one concern also controls another concern. For example, if the CEO (or other officers, managing members, or partners) of one business also control the management of another business, those businesses will be affiliates for size purposes because the same management controls both businesses.

Significantly, affiliation also arises where a single individual, concern, or entity controls the management of the applicant concern through a management agreement.

- Affiliation Based on Identity of Interest

"Identity of interest" affiliation "may arise" among two or more firms that are economically dependent on each other through close business relationships or that have identical or substantially identical business or economic interests.

For example, identity of interest affiliation is frequently found between businesses owned by close relatives if the businesses show identical economic interests, such as operating similar businesses in the same or similar industry in the same geographic region. Identity of interest affiliation also may arise based on common investments where the same individuals or firms together own a substantial portion of multiple concerns in the same or related industries or where those similar businesses share resources, equipment, locations, or employees.

Identity of interest affiliation based on economic dependence also "may arise" when a concern derived 85 percent of its receipts over the three previous fiscal years from a contractual relationship with another concern, unless the relationship meets certain exceptions.

Significantly, unlike the stock ownership and common management bases of affiliation discussed above, when a presumption of identity of interest affiliation exists, applicants may rebut that presumption with evidence showing that the interests deemed to be one are in fact separate. In SBA contract cases that have regulations similar to the loan program, this is proven by showing a "clear line of fracture" between the concerns.Size Appeal of: Alleo Corp., SIZ-5405 (Sept. 26, 2012).

- Affiliation and Angel Investors – Potential Issue of Negative Control

The SBA Business Loan affiliation rules also provide that "SBA will deem a minority shareholder to be in control, if that individual or entity has the ability, under the concern's charter, by-laws, or shareholder's agreement, to prevent a quorum or otherwise block action by the board of directors or shareholders."

Several investor term sheets include certain provisions to protect the investment. For example, angel investors often require the founders of the business to obtain the angel investor's consent before liquidating or dissolving the company, entering into a merger or similar transaction, or before the filing of bankruptcy. When evaluating negative control provisions to determine whether affiliation exists, the key question is whether the provisions cover "extraordinary actions" necessary to protect the investment or just ordinary business decisions. The investor will be deemed to control the concern if supermajority consent is required for ordinary business decisions.

SBA Office of Hearings and Appeals (SBA OHA) size decisions, which decide cases based on the very similar affiliation regulations at 13 C.F.R. § 121.103 related to small business set-aside contracts, frequently hold that negative control by an investor does not create affiliation if the negative control only blocks certain "extraordinary actions." Affiliation does not arise if the supermajority provisions are crafted to protect the investment of minority shareholders, and do not impede the majority's ability to control the company's operations or to conduct the company's business as it chooses.

For example, in Size Appeal of: Southern Contracting Solutions III, LLC, SIZ 5956 (Aug. 30, 2018), SBA OHA closely evaluated an operating agreement and determined that a long list of supermajority provisions requiring unanimous consent of all the members did not give rise to affiliation based on negative control because they covered extraordinary actions intended to protect the investment of minority shareholders. The supermajority provisions addressed in Southern Contracting Solutions III, LLC included supermajority approval for:

- The sale of all or substantially all assets of the company;

- A mortgage or encumbrance upon all or substantially all assets of the company;

- Any matter which could result in a change in the amount or character of the company's contributions to capital;

- A change in the character of the business of the company;

- A false or erroneous statement in the articles of organization;

- Disposal of the goodwill of the company;

- Submission of claim of the company to arbitration;

- Confession of a judgment;

- Commission of any act which would make it impossible for the company to carry on its ordinary course of business;

- Amendment of this operating agreement; or

- Amendment of the articles of organization to change the management of the company from the member to managers or from managers to members.

Therefore, relying on these relevant OHA decisions interpreting the set-aside contract programs, applicants have very good arguments that this same analysis of supermajority provisions should be applied to the loan programs. Supermajority provisions blocking extraordinary actions should not give rise to affiliation between a minority investor and the applicant. However, the above provisions related to ownership, management, and identity of interest would still apply.

Beyond the above, the SBA can also find affiliation based on a totality of the circumstances and other relationships between parties. Businesses should evaluate these regulations to identify their own affiliates.

Affiliation Exceptions in the COVID-19 Loan Programs

Affiliation principles apply to the EIDL program as described in 13 C.F.R. § 121.301, et. seq. and 13 CFR 123.300, et. seq. The PPP in the CARES Act expressly waives the affiliation analysis for:

- Any business in accommodation and food services industries (NAICS Code starting with "72") with not more than 500 employees as of the date on which the loan is disbursed.

- Any business concern operating as a franchise that is assigned a franchise identifier code by the SBA. The list of entities that currently have a SBA franchise identifier code can be found in the SBA Franchise Directory.

- Any business that receives financial assistance from a Small Business Investment Corporation (SBIC). SBICs are privately owned and managed investment funds that are licensed and regulated by the SBA and use their own capital, plus funds borrowed with an SBA guarantee, to make investments in small businesses. SBA's current affiliation rules already confirm that business concerns owned in whole or substantial part by SBICS are not considered affiliated with such SBICS. Also, financial assistance from an SBIC is regulated by 13 C.F.R. § 107.20, et. seq., which is different than the SBA Business Loan regulations upon which the PPP is based. Therefore, we will need to wait for the SBA regulations to determine whether SBA interprets this exception as a simple restating of the current affiliation exceptions related to SBICs or some new exception that will allow businesses to get additional assistance related to the PPP.

Outside of the above exceptions, the affiliation analysis should apply when determining size for both the EIDL and the PPP loan programs.

Applying These Principles to Loan Eligibility

As we previously discussed in an alert on March 24, 2020, the EIDL loans that are distributed directly by SBA are now available and businesses can start applying for those loans here.

When evaluating eligibility for those loans, businesses should consider the following regulations to evaluate eligibility under the applicable size standards while also considering applicable affiliation requirements 13 C.F.R. 121.301, et. seq. and 13 CFR 123.300, et. seq.

The PPP loans, which will be distributed by banks, are not yet available as final rules are still being implemented by SBA. However, as we previously discussed here, the basic eligibility requirements have been issued and businesses would be wise to contact their lenders to express their interest now.

Once the SBA regulations are finalized for the PPP provisions of the CARES Act, we will better understand how the SBA will apply the affiliation and size standard principles referenced in this alert.

Resources

Previous Baker Donelson alerts:

Other resources:

Baker Donelson is working hard to assist clients in these unprecedented times. Our team of attorneys and advisors continue to monitor and advise on new issues as they develop. For specific guidance or more information on this alert, please contact D. Jeffrey Wagner. For more information and general guidance on how to address legal issues related to COVID-19, please visit the Coronavirus (COVID-19): What you Need to Know information page on our website.